| Summary of 2025 TRS Net Zero Actions |

| DISCLOSE Emissions and Risk |

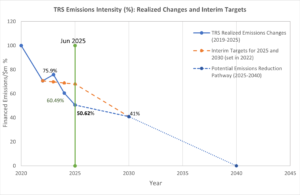

| As of June 30, 2025, for the public markets, TRS’ Scope 1 and 2 financed emissions intensity was 43 tons of financed emissions / million dollars invested (FE/$m), marking a decrease of 16% from June 30, 2024. Compared to the December 31, 2019, baseline, TRS has observed a reduction of 49% in Scope 1 and 2 financed emissions intensity, against an interim target of 32% reduction by June 2025. TRS had surpassed its interim emissions reduction target for Scope 1,2 intensity for public equity and corporate bonds a year earlier in 2024, and has continued to decrease the footprint in FY2025 |

| As of June 30, 2025, TRS’ Scope 3 financed emissions intensity was 253, marking a decrease of 19% from June 30, 2024. |

| Active equity explains majority of the decrease in emissions for both Scopes 1 and 2 and Scope 3 for TRS in FY2025. |

| ENGAGE for Alignment and Action |

| In the last three years, BAM has engaged with over 100 companies on climate change. |

| By the end of fiscal year 2025, approximately 27% of the System’s financed emissions are covered by validated targets.

This figure is inclusive of the financed emissions of companies with targets validated by Science-Based Targets Initiative (SBTi) and the Global Steel Climate Council (GSCC) standard as well as those with commitments to have targets validated through either organization |

| In addition to engaging across the portfolio on science-based targets and other general decarbonization topics, TRS also works at a sector and systemic level to engage with high-priority industries and on critical cross-sectoral issues including focusing on utilities, hyperscalers and data centers, and the largest banks on the energy supply ratio.

The TRS Net Zero Implementation Plan included the exploration of alternative frameworks to measure and monitor the state and progress of net zero alignment of portfolio companies. In 2025, BAM implemented the alignment assessment for the Sytem’s listed equity and corporate fixed income portfolios using the NZIF 2.0, developed by Paris Aligned Investment Initiative (PAII). |

| All TRS’s 42 public markets managers submitted plans to align with the System’s net zero goal by adopting a net zero goal, science-based targets or acceptable alternative approach to support a transition to a net zero economy.

A substantial majority, or 64%, of the System’s public markets managers adopted net zero goals and/or quantified engagement or portfolio targets that apply to the System’s investments. A substantial majority, or 69%, of the System’s public markets managers created new policies or practices or enhanced existing policies or practices to support decarbonization of their portfolio companies and assets as a result of the System’s net zero expectations. |

| INVEST in Climate Change Solutions |

| As of 6/30/25, TRS has a total of $7.34 billion in invested and unfunded commitments in climate change solutions across all asset classes, after having surpassed the interim goal of $4.2 billion by 2025 in FY 2024. The 2035 goal remains $19 billion.

BAM is reviewing strategies to maximize the impact of climate solution investments to advance TRS’s net zero goals while delivery superior risk-adjusted financial returns. |

Section 1: Disclose Emissions and Risks

1.1. Public Equity and Corporate Bonds Interim Scope 1 and 2 Emissions Reduction Progress

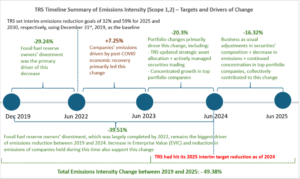

The emission intensity for TRS decreased during FY 2025, after surpassing the interim emission reduction target set for Jun 30, 2025. TRS’ Scope 1 and 2 financed emissions intensity decreased by 16% between Jun 30, 2024, and June 30, 2025, yielding a total reduction of 49% from the baseline of Dec 31, 2019. While we welcome this decrease in our portfolio’s footprint, it is important to understand and acknowledge the drivers of this change: most of this emission reduction is driven by portfolio and market changes (including changes in securities’ weight and increase in the valuation of companies) while actual company emission decreased as well. (See Section 1.2 for more detail on the attribution analysis.)

In our Net Zero Implementation Plan, TRS set targets to reduce the Scope 1 and 2 financed emissions intensity in our public equity and corporate bonds portfolio (including investment grade, high yield and convertible bonds) by 32% by 2025, 59% by 2030, and 100% by 2040, using a baseline of December 31, 2019. For these interim emissions reduction targets, TRS uses “financed emissions intensity” (tons of CO2 equivalent emissions/$million invested) based on Enterprise Value Including Cash (EVIC) as the primary metric for emissions. We also report, measure and evaluate changes in absolute financed emissions (which will be also referred to as financed emissions or FE in this report) and weighted average carbon intensity (WACI) (tons of CO2/$million sales) and strive toward comparable progress among all metrics. Scope 3 emissions and target-setting are discussed in the subsection further below. For definitions of Scopes 1, 2 and 3, please see Appendix A.

1.2. Public Equity and Corporate Bonds Annual Carbon Footprint Analysis

On behalf of TRS, BAM conducted an annual updated carbon footprint analysis of the System’s public equity and corporate bond portfolios and a blended benchmark portfolio. We do not yet have complete and accurate enough data for measuring greenhouse gases (GHGs) emissions in private markets. The analysis used holdings data as of June 30, 2025, and MSCI’s carbon footprint data and analytics (which includes PCAF-aligned metrics for 2025)[1]. Public equity and corporate bonds constituted 60% of TRS’ total assets as of June 30, 2025. Corporate bonds include investment grades and high yields.

1.2.1. Scope 1 and 2 – Financed Emissions and Intensity

During Fiscal Year (FY) 2025 TRS’ public portfolio emissions intensity experienced a much greater reduction than the blended benchmark, as depicted in Table 1. Most of this decrease was driven by portfolio level changes: business as usual changes in the actively managed securities and highly concentrated expansion of low carbon intensity companies (e.g., the Magnificent Seven) in TRS’ portfolio value. It also helped that overall emissions in developed economies decreased in 2024[2].

TRS’ public equity and corporate bonds’ absolute financed emissions also decreased more than that of the benchmark during FY 2025. Actively managed equities accounted for most of the reduction in TRS. However, the financed emissions in the fixed income portfolios increased during this time. For the more detailed breakdown of Scope 1 and 2 financed emissions by asset class, see Appendix B.

Table 1: Public Equity and Corporate Bonds Scope 1 and 2 Financed Emissions Intensity and Absolute Financed Emissions

| TRS – Financed Emissions Intensity – Scope 1 and 2 | ||

| TRS Portfolio Tons carbon emissions/$m invested |

Blended Benchmark Tons carbon emissions/$m invested |

|

| 31-Dec-19 | 84.20 | 79.95 |

| 30-Jun-22 | 59.58 | 60.70 |

| 30-Jun-23 | 63.90 | 71.40 |

| 30-Jun-24 | 50.93 | 62.06 |

| 30-Jun-25 | 42.62 | 53.54 |

| Change % (2019-2025) | -49.38% | -33.03% |

| Change % (2024-2025) | -16.32% | -13.73% |

| TRS – Absolute Financed Emissions – Scope 1 and 2 | ||

| TRS Portfolio Tons carbon emissions |

Blended Benchmark Tons carbon emissions |

|

| 31-Dec-19 | 3,530,313 | 3,844,317 |

| 30-Jun-22 | 2,786,341 | 2,823,438 |

| 30-Jun-23 | 3,349,152 | 3,744,197 |

| 30-Jun-24 | 3,117,777 | 3,786,283 |

| 30-Jun-25 | 2,916,084 | 3,663,237 |

| Change % (2019-2025) | -17.40% | -4.71% |

| Change % (2024-2025) | -6.47% | -3.25% |

Like previous years, the highest emitting sectors in TRS’ portfolio are materials, utilities, energy, and industrials based on the Global Industry Classification Standard categorization, collectively representing almost 82% of financed emissions for Scope 1 and 2, as reported in Table 2 below. On behalf of TRS, BAM is actively engaging with portfolio companies in these high-emitting sectors (see more details in the engagement section).

Table 2: High Emitting Sectors – Financed Emissions (Scopes 1 and 2)

| TRS Portfolio – High Emitting Sectors’ Financed Emissions (Scope 1 and 2) | ||

| 2025 | 2024 | |

| Materials | 30% | 34% |

| Utilities | 27% | 25% |

| Industrials | 13% | 11% |

| Energy | 12% | 12% |

| Top 4 Sectors Share in Absolute Financed Emissions | 82% | 82% |

Figure 1 below shows the percentage of Scope 1 and 2 emissions reductions pathways for the public equity and corporate bonds portfolios each year to achieve the interim emissions reduction targets of 2025 and 2030 and net zero emissions by 2040. If we assume a linear emission reduction pathway, TRS had surpassed the 2025 emissions reduction targets ahead of schedule (in 2024) and has continued to see further reduction in FY2025. We caveat that the emission reduction pathway required for the whole real economy to reach net zero by 2050 is nonlinear.[3] Figure 2 summarizes the timeline and drivers of emissions intensity changes between 2019 and 2025.

Fig 1: TRS – Realized and Projected Emissions Reduction Targets (Scope 1 and 2)

Fig 2: TRS – Timeline of Emissions Intensity (Scope 1 and 2)

– Milestones and Drivers of Change

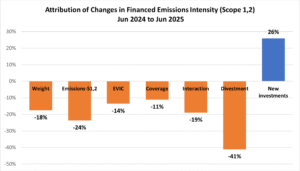

1.2.2. Scope 1 and 2 Attribution Analysis of Financed Emissions

Last year, to further our understanding of the drivers of reduction in this emissions intensity between 2019 and 2024, we conducted a detailed attributional analysis[4] by separating the effect of each factor that affects the emissions intensity calculation one factor at a time from 2019 to 2024, assuming everything else is held constant. These factors include changes in portfolio positions, changes in coverage of emission data, changes in emissions in the real economy, etc. The analysis identified fossil fuel divestment as the biggest driver of emission reduction between 2019 and 2024. We conducted a similar attribution analysis for FY2025. To analyze the contribution of changes in financed emissions from portfolio position changes, we looked at these areas:

- Sales of investments: securities in the portfolio in 2024, but not in 2025. These sales are driven primarily by business-as-usual changes in actively managed accounts in the TRS portfolio.

- New investments:securities that were not in the 2024 portfolio but are held in the 2025 portfolio.

- Securities that were held between FY 2024 and FY 2025: for these securities, we broke down the marginal effects of changes in individual factors (company emissions, EVIC, weight, and portfolio coverage) that changed portfolio financed emissions. The interaction term captures the residual portion that cannot be explained by changing factors individually.

Figure 3 summarizes the findings of the attribution analysis. Business as usual changes (buying and selling of securities) had the largest effects on financed emission changes in FY2025. Changes in companies’ valuation/EVIC and decrease in actual company emissions also affected the drop of financed emissions.

Fig 3: TRS – Attribution Analysis of Change in Emissions Intensity (Scope 1 and 2)

– Jun 2024 to Jun 2025

1.2.3. Scope 3 – Financed Emissions and Intensity

During FY 2025, TRS’ Scope 3 public portfolio emissions intensity experienced a much greater reduction than the blended benchmark, as depicted in Table 3.

The absolute financed emissions of TRS’ public equity and corporate bonds also decreased more than that of the benchmark during FY 2025. Actively managed equities accounted for most of the reduction in TRS Scope 3 financed emissions during FY 2025, while fixed income related financed emission increased during this time. For the more detailed breakdown of Scope 3 financed emissions by asset class, see Appendix C.

Table 3: Public Equity and Corporate Bonds Scope 3 Financed Emissions and Intensity

| TRS – Financed Emissions Intensity – Scope 3 | ||

| TRS Portfolio Tons carbon emissions/$m invested |

Blended Benchmark Tons carbon emissions/$m invested |

|

| 30-Jun-22 | 241.80 | 379.00 |

| 30-Jun-23 | 346.90 | 431.90 |

| 30-Jun-24 | 311.08 | 393.75 |

| 30-Jun-25 | 252.60 | 343.90 |

| Change % (2024-2025) | -18.80% | -12.66% |

| TRS – Absolute Financed Emissions – Scope 3 | ||

| TRS Portfolio Tons carbon emissions |

Blended Benchmark Tons carbon emissions |

|

| 30-Jun-22 | 11,346,047 | 17,625,211 |

| 30-Jun-23 | 18,190,595 | 22,644,318 |

| 30-Jun-24 | 19,042,557 | 24,023,944 |

| 30-Jun-25 | 17,283,032 | 23,529,829 |

| Change % (2024-2025) | -9.24% | -2.06% |

1.2.4. Decision Around Target Setting on Scope 3 Financed Emissions

The System’s Net Zero Implementation Plan created in 2023 committed BAM to “annually measure, assess and report progress in Scope 3 emissions beginning with 2022 data, with a focus on high emitting sectors and sectors and companies where Scope 3 is material” and to “set interim Scope 3 emissions reduction targets by 2025 as data availability and quality improve.” Investors have focused on Scope 3 emissions because they capture the emissions coming from companies’ whole value chain, whether from upstream (e.g., extraction, processing, manufacturing, transport and distribution for a consumer-electronics company) or downstream emissions (e.g., the lifetime emissions of vehicles sold by an automotive company). Scope 3 emissions can represent over 90% of a company’s Scope 1, 2, and 3 emissions.[5]

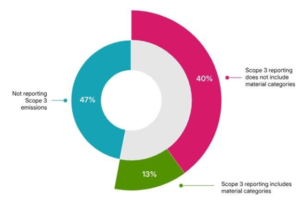

For Scope 3 data to guide BAM’s corporate engagement and communicate status and progress to our stakeholders, they need to accurately represent emissions in portfolio companies’ value chain, and changes in the data need to represent efforts that portfolio companies or BAM makes vs factors outside of companies’ or our control. Unfortunately, at this point, Scope 3 data do not meet these criteria. Reported Scope 3 data are limited, have a high degree of estimation, and cover few of the material categories. The graph below illustrates these points.[6]

Given the current sparse reporting of Scope 3 emissions, changes in the data could come from an increased number of companies reporting their emissions differently than the previously estimated data by data providers, increased categories that companies report, or actual changes in Scope 3 emissions. Only the last category is meaningful for BAM’s objectives.

Another challenge with Scope 3 emissions at a portfolio level is the same emissions by a real economy activity can be counted multiple times. Using a portfolio containing a carmaker, an oil & gas company, a car leasing company, and a bank providing financing for all three companies above as an example, the emissions from driving a car will be captured by the Scope 3 emission of the carmaker, the oil & gas company, the car leasing company, and the bank. The Scope 3 emissions of the bank would capture the Scope 1, 2, and 3 emissions of the three real economy companies. Setting Scope 3 targets at a portfolio level could lead to unintended actions that are not necessarily the best outcome to reduce real economy emissions.[7]

Recognizing these challenges, the guidance on Scope 3 emissions by Net Zero Asset Owner Alliance and the Net Zero Investment Framework developed by the Paris-Aligned Investor Initiative does not require target-setting on Scope 3 emissions and suggest reporting Scope 3 data separately from that of Scope 1 and 2. The practices around Scope 3 emissions of multiple asset managers surveyed by BAM are consistent with the guidance.

There are alternative metrics to capture the emissions associated with companies’ value chain. For downstream emissions that are material to sectors such as extractive mining and automakers, these metrics could be low-carbon product mix, use phase efficiency, and customer engagement metrics. For upstream emissions that are material to sectors such as retailers and food producers, these metrics could be percentage of recycled materials used, energy intensity of purchased goods, and percentage procurement from low-emission suppliers.

BAM commits to explore the most effective ways to reduce Scope 3 emissions in 2026. We plan to engage with market leaders and peer asset owners on what is needed to make disclosure of and manage material categories of Scope 3 emissions a market standard. We will do more systematic Scope 3 engagement after we understand the best practices and our ability to effect change.

Section 2: Public Portfolio Company Engagement

TRS’s Net Zero Implementation Plan articulates the core role that corporate engagement plays in reaching Net Zero. TRS intends to be a partner with portfolio companies throughout their journey to net zero.

In the last three years, BAM has engaged with over 100 companies on climate change. It was the first time that BAM engaged with most of these companies on any issue.

2.1. Science-Based Target Goal

In the Net Zero Implementation Plan, TRS set an interim goal of 70% of scopes 1 and 2 financed emissions to be covered by science-based targets by FY 2025. This goal has not been met. By the end of FY 2025, approximately 27% of the System’s financed emissions are covered by validated targets.

This figure is inclusive of the financed emissions of companies with targets validated by Science-Based Targets Initiative (SBTi) and the Global Steel Climate Council (GSCC)[8] standard as well as those with commitments to have targets validated through either organization. TRS evaluated GSCC and determined it meets its needs as a robust target setting protocol given both its methodological design and requirement for third-party validation.

Several factors prevented the adoption of acceptable science-based targets among the highest emitting companies, including the lack of validating entities beyond SBTi, the lack of protocol for high-emitting sectors, and ongoing political challenges. In 2025, BAM on behalf of TRS submitted comments to SBTi during its public consultation for its revised Corporate Net Zero Standard (CNZS). It is BAM’s view that while SBTi remains best-in-class for target setting, it is unfortunately not well-suited for use by the highest emitting companies and sectors, particularly those in North America. An excerpt from TRS’s comments on the first public consultation for the revised standard states:

Currently, there is limited SBTi adoption among companies in the most critical sectors. Many such companies currently have voluntary net zero commitments that are not validated or backed with science-based interim targets, which weakens the meaning of net zero and does not facilitate progress towards limiting global temperature rise. The proposed revisions to the [Corporate Net Zero Standard] CNZS and its relationship to the sector-specific standards will likely make this situation more pronounced.

As written, it is unlikely that the highest emitting large companies… will utilize this standard.

Given the trust that SBTi has among investors and other stakeholders, identifying a way to grow the tent rather than shrink it is critical to achieving the economy-wide results that are necessary to limit global temperature rise.

We still believe that setting and managing to targets that are aligned with 1.5 degree and well-below 2 degree goals are critically important actions for a company to take. Our expectation remains that portfolio companies will set science-based targets, but TRS is adjusting its approach because of the reality on the ground.

Given the limitations of the SBTi framework for the highest emitting companies in 2025, TRS began reviewing additional ways to evaluate and differentiate among portfolio companies using other metrics and assessments with the Net Zero Investment Framework being one of them.

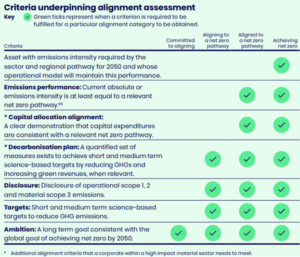

2.2. Net Zero Investment Framework (NZIF)

The TRS Net Zero Implementation Plan included the exploration of alternative frameworks to measure and monitor the state and progress of net zero alignment of portfolio companies. In 2025, BAM implemented the alignment assessment for the Sytem’s listed equity and corporate fixed income portfolios using the NZIF 2.0, developed by Paris Aligned Investment Initiative (PAII). For these markets, the graph from PAII below shows the criteria underpinning the NZIF alignment assessment:

BAM chose to implement this alignment assessment for a few reasons:

- The NZIF framework captures a range of actions companies can take to decarbonize beyond science-based targets, which BAM can engage on. For example, a company could have capex spending on decarbonization without setting short- and medium-term science-based targets. Using this framework, BAM has compiled and analyzed decarbonization actions leading companies in a sector are taking and can use the information to engage with other companies in the same sector. TRS expects that this will allow for focused engagement around topics specific to one sector. TRS will also be able to differentiate at a more granular level among peer companies.

- Many asset managers have developed in-house alignment assessment methodologies using the NZIF framework to support their investment and engagement. The framework is also widely used by peer asset owners.

- The NZIF framework is consistent with other key assessments such as the Climate Action 100+ Net Zero Company Benchmarkand Climate Engagement Canada Net Zero Benchmark. Holistically, the components of this framework are already covered in collective engagements.

The NZIF guidance states that “NZIF outlines the key components of a net zero strategy and transition plan that an investor can consider… It is only a guide, not a prescriptive protocol, nor a standard, and it is not a reporting framework.” For example, there is no widely accepted definition of what a good decarbonization plan is, or how to measure capital allocation alignment. Data on companies’ targets and capex is generally lacking. The criteria described above are most suitable for higher-emitting sectors, not so much for pure play renewable or electric vehicle companies, such as Orsted and Tesla Orsted and Tesla do not set climate targets or disclose their emissions, which would disqualify them from being assessed as “Achieving Net Zero” even when their emission intensity meets the net zero pathways.

In next year’s Annual Climate Report, we plan to communicate specific engagement goals and targets to supplement existing targets.

2.3. Ongoing Systemic and Sectoral Engagement

In addition to engaging across the portfolio on targets and other general decarbonization topics, TRS also works at a sector and systemic level to engage with high-priority industries and on critical cross-sectoral issues.

2.3.1. Engagement on Utilities

Utilities remain a critical lynchpin to economy-wide decarbonization. For FY 2025, utilities were responsible for approximately 27% of TRS’s financed emissions. For two years, BAM served as a stakeholder advisor to the Electric Power Research Institute’s (EPRI) effort to design an alternative target setting methodology called SMARTargets. During that period, BAM also served as lead investor for the topic of science-based targets among Climate Action 100+ (CA100+) signatories primarily to engage with the highest emitting US utilities on targets and other topics and is now the CA100+ co-lead investor for engagement with American Electric Power (AEP). BAM has assessed that EPRI SMARTargets is unfortunately not likely to fill the need for a decision-useful target-setting protocol that produces validated targets aligned with pathways that limit warming to 1.5 degrees and could present an unacceptable greenwashing risk. In comments to SMARTargets during the public consultation process, BAM articulated several of the core issues:

As large, diversified funds with broad exposure across the global economy, [TRS has] direct economic interest in the overall strength of the financial markets and broader economy in which [we] invest. With obligations to our beneficiaries that extend for decades, we are obligated to attend to long-term risks and opportunities. We have a fiduciary duty, therefore, to protect against downside and systemic risks and foster stable financial markets and long-term economic growth essential to the performance of [TRS’s] investments. [TRS] has in place a set of plans and policies reflective of our Investment Belief that our role as a fiduciary obligates us to “mitigate the risks, take advantage of opportunities, and reduce the contributions our investments make to climate change.” One such policy, in line with our fiduciary obligation, is a short-term goal for the highest emitting public portfolio companies to set science-based emissions reductions targets to “increase[e] the alignment of our investments with science-based pathways to limit global warming to 1.5⁰ C.”

The science-based methodology that SMARTargets puts forth is not consistent with this approach. SMARTargets integrates climate science findings with a company’s economic and business considerations under the umbrella of scientific rigor. This could result in misleading claims of alignment with science and be challenging for stakeholders who are assessing targets based on the targets’ climate alignment.

While we agree that economic efficiency is important and understand that utilities need to manage issues of affordability, reliability, equity, and resiliency within particular regulatory frameworks, the starting-point of a standardized methodology to develop targets should be emissions reductions …SMARTargets fundamentally redefines what constitutes “science-based” methodology by incorporating economic considerations as scientific requirements… [examples include SMARTargets approach to] “[a]ccounting for and informing the multiple social priorities that a company is responsible for beyond decarbonization, such as affordability and reliability” and [c]onsidering “differences in decarbonization opportunities due to differences in, among other things, assets, markets, regulatory structure.” These are fundamentally economic and business considerations, not climate science findings. Yet SMARTargets presents them as emerging from “assessment of all the relevant science” and labels them as “scientific requirements.”

TRS continues to expect its portfolio companies to set science-based emissions reductions targets. In October 2025, then-Comptroller Brad Lander convened a roundtable focused on addressing the need for a mutually agreeable framework for setting and assessing emissions reductions targets in the utility sector. This roundtable was attended by over 60 institutions with representation from asset owners, asset managers, utilities, and service providers.

There are some strong and positive elements to EPRI SMARTargets, such as the focused transition planning process, and there seems to be opportunity for alignment around different metrics and assessments. In 2026, TRS engagement will focus on the identification of metrics that demonstrate interim goals, which their investors can track. BAM is also working with nonprofits and research entities (such as Rocky Mountain Institute, Center for Climate and Energy Solutions, etc.) to assess a company’s existing disclosures and to determine how future SMARTargets outputs, disclosed as part of a formal SMARTargets process, might allow investors to track portfolio companies’ emissions trajectories and emission reduction targets.

Utilities face significant challenges as they decarbonize because of the exponential load growth driven by AI, reshoring, and electrification. TRS remains concerned about utilities’ greenwashing and representing their targets in a way that is inconsistent with global consensus definitions and frameworks, which poses reputational and litigation risks. TRS will continue to address these risks with our portfolio companies through engagement.

2.3.2. Engagement on Data Centers and AI

TRS is increasingly concerned about the increasing carbon emissions of and electricity costs caused by AI-driven data centers and is engaging with both utilities and increasingly with hyperscalers on this issue. In their own 2025 disclosures, the largest technology companies reported significant increases in emissions in the last several years. For example:

- In 2025, Microsoft reported a 23.4% increase in emissions since 2020.[9]

- Amazon reported its first emissions increase since 2021(+6%).[10]

- Google reported that its “ambition-based emissions” grew 11% in 2025, which is a 51% increase compared to 2019.[11]

TRS will be engaging with the largest tech companies on this alarming trend and are calling on these companies to disclose additional information to their investors. We expect companies to take all steps, including during contracting, to protect ratepayers, shareholders, and live up to their climate commitments in a way that does not result in economy-wide emissions increases.

2.3.3. Engagement on Banks

In 2025, TRS also continued its engagement with the largest North American banks on the Energy Supply Ratio. After reaching a settlement with TRS in 2024 concerning TRS’ shareholder proposal, JP Morgan and Citigroup disclosed their energy supply ratios and methodologies. JP Morgan and Citigroup used vastly different approaches in designing the methodology for their energy supply ratio, reflective of the two banks’ different approaches to disclosures and managing risk associated with those disclosures.

- As a result of different design choices, the published Ratios are not comparable to one another.

- JP Morgan’s choices led to the publication of a ratio that paints the bank in a more favorable light from a climate perspective, while Citi went the opposite direction. In fact, while JPM’s self-published ratio is higher than its Bloomberg New Energy Finance-calculated ratio, Citi’s is lower.

In the next year, investors will be able to track each bank’s progress against its own previously published ratios but will not be able to use these disclosures to compare peers. Royal Bank of Canada (RBC), who also reached settlement with TRS in 2024, was unable to disclose its ratio but did disclose its methodology for constructing its ratio.

In 2025, TRS re-filed proposals at Bank of America, Goldman Sachs, Morgan Stanley, and Wells Fargo. At Bank of America, the proposal received 16.4% of the vote, at Goldman Sachs 15.1%, at Morgan Stanley 13%, and at Wells Fargo 18%.

Section 3: Asset Managers Engagement: Net Zero Plans by 2025

TRS’ Net Zero Implementation Plan set expectations for our asset managers to align as best as possible with the System’s net zero goal:

- Public markets asset managers were expected to have a net zero goal, science-based targets, or acceptable alternative approach to support a transition to a net zero economy, and an implementation plan covering, at a minimum, assets managed for the System, by June 30, 2025, and submit summary plans for their goals and strategies by that date.[12]

- Private markets managers are expected to meet the same expectations for commitments TRS makes from July 1, 2026, onward.

3.1 Summary of Assessment of Public Markets Asset Managers’ Plans

By June 30, 2025, all of TRS’ 42 public markets managers submitted plans to align with the System’s net zero expectations. This successful response followed extensive engagement of all public markets managers by BAM beginning in 2023 continuing through 2025. During this time, BAM communicated with all of TRS’ current managers, in writing and through meetings, to ensure they were aware of the Systems’ Net Zero by 2040 expectations and encourage them to align with the expectations, consistent with fiduciary duty and their investment objectives. In addition, in April 2025, BAM sent guidance to all public markets managers highlighting key elements to consider as they developed their goals and plans. Please see further below for a summary of this guidance.

BAM closely reviewed and assessed every manager’s plan to evaluate how well they align with the System’s net zero expectations, considering differences across managers and their investment strategies. For most managers, BAM held individual meetings to provide feedback and ask clarifying questions to support them in improving their plans. BAM also engaged managers on how their plans were consistent with fiduciary duty and the objective of delivering optimal investment performance for the System’s beneficiaries.

Based on BAM’s initial assessment in 2025, 93% (39 of 42) of public markets managers’ plans were aligned with the System’s net zero expectations. BAM initially assessed three managers as insufficiently aligned: BlackRock, Fidelity, and PanAgora. However, PanAgora has since strengthened their approach to engaging portfolio companies to better align with the System’s expectations. Hence, as of the publication of this report, 40 of 42 managers are assessed as aligned while BlackRock and Fidelity are still assessed as insufficiently aligned.

In November 2025, then-Comptroller Lander submitted a memorandum[13] to the Board of Trustees of the System providing the rationale for the assessment of BlackRock and Fidelity and recommending that the System put BlackRock’s mandates for U.S. equity index funds totaling $25.3 billion out to bid, and that TRS terminate Fidelity’s World ex-US small cap mandate of $384 million.

3.1.1. Summary of BAM’s Assessment Framework

BAM assesses managers’ plans primarily on whether they have a systematic approach to engage portfolios companies to drive real economy decarbonization in line with best available science on achieving the 1.5° C ambition of the Paris Agreement where feasible and consistent with fiduciary duty. BAM’s guidance to managers emphasizes this core expectation:

Asset managers should not exclude or select investments (portfolio companies or assets) for the purpose of meeting these expectations unless doing so is fully consistent with the manager’s fiduciary duty and the relevant fund’s investment objectives and standards. The Systems seek to support real economy decarbonization which cannot be achieved through portfolio decarbonization alone but requires broad engagement of investments to appropriately transition.

In addition, BAM does not seek a single approach for all managers but evaluates what is appropriate based on asset class, investment strategy, industry, geography, market factors, resources and other characteristics of the asset manager, portfolio companies and underlying assets.

BAM also encourages managers to consider established industry frameworks on net zero alignment such as the STBi, NZIF, CA100+ Net Zero Company Benchmark, Transition Pathway Initiative (TPI), Net Zero Aset Owners Alliance (NZAOA) publications, and the Private Markets Decarbonization Roadmap (PMDR)[14]. Many of the System’s managers use, or have begun to use, one or more of these frameworks to inform their approach to decarbonization.

BAM assesses managers based on key elements highlighted in BAM’s guidance. First, BAM assesses whether the manager has a net zero goal or science-based targets that apply to the System’s assets. If the manager has such a goal or targets, BAM will generally view the manager as aligned with the System’s expectations but will continue to assess the manager on whether it demonstrates a systematic approach to stewardship. BAM also assesses every manager on whether they incorporate material climate change-related risks and opportunities in investment-decision making, including due diligence and portfolio management.

Second, if the manager has not adopted a formal net zero goal or science-based targets, BAM will assess whether the manager has an acceptable alternative approach to support a transition to a net zero economy. In this assessment, BAM places particular weight on the manager’s approach to stewardship given the emphasis of the System’s net zero expectations on real economy decarbonization. Specifically, BAM assesses the following aspects of managers’ stewardship and engagement approaches:

- Focus List and Engagement Target: Does the manager have a clear rationale and process for identifying companies to prioritize for engagement (e.g. creating a focus list)? Does the manager have a quantified portfolio coverage target such as the NZIF-recommended target of 70% of financed emissions (Scope 1 & 2) of investments managed on behalf of the Systems increasing to 90% of financed emissions (Scope 1, 2 & material 3) by 2030?

- Systematic Engagement on Climate Practices: Does the manager have a systematic approach to engage companies to achieve continuous improvement in their practices to address climate risks and opportunities? Does the manager consider engaging companies to adopt the following important climate practices?

| Governance | Emissions Measurement | Quantified Climate Ambition |

| Transition Plan | Capital Expenditures Alignment | Performance on climate goals |

| Climate Risk Disclosures | Lobbying Alignment | Just Transition |

BAM expects, and communicates with managers, that portfolio companies will increase and improve their climate practices on different timelines and paces. While it is not expected that all companies will necessarily be able to adopt all the climate practices during the manager’s holding period, BAM encourages managers to make best efforts to encourage companies to be on a pathway to adopting all the practices.

BAM also assesses how managers monitor portfolio companies’ progress, consider escalation measures when engagement is not successful, and have a coherent proxy voting policy as it relates to climate. Lastly, BAM assesses the manager’s willingness to provide annual reporting on engagement activities conducted under the plan. As of the writing of this report, BAM is in the process of finalizing more detailed guidance on how managers can provide annual reporting on their climate-related engagement activities.

When a manager lacks an approach on any of the elements summarized above, BAM engages the manager to seek clarification and encourages the manager to adopt an appropriate policy or practice. Virtually all managers have been responsive and willing to develop new practices, as needed, to meet the System’s expectations, consistent with fiduciary standards.

3.1.2. Highlights of Public Markets Managers Net Zero Alignment Approaches

Substantial Majority of Managers Adopted a Net Zero Goal, Science-Based Targets, and/or Quantified Targets to Support a Net Zero Economy

As described above, the System set expectations for managers to adopt a net zero goal, science-based targets, or acceptable alternative approach to support a transition to a net zero economy. Where a manager does not have a formal net zero goal or science-based target, they are expected to demonstrate a systematic approach to stewardship on decarbonization including a clear process for prioritizing companies for engagement and systematically engaging companies toward continuous improvement on decarbonization practices.

Best practice for this includes adopting quantified targets for engagement and/or portfolio net zero alignment. As noted earlier, BAM specifically encourages managers to consider a quantified portfolio coverage target of 70% of financed emissions (Scope 1 & 2) of investments managed on behalf of the Systems, increasing to 90% of financed emissions (Scope 1, 2 & material 3) by 2030. These targets may also include goals to increase the percentage of the portfolio that is advanced on decarbonization. This is consistent with guidance of NZIF.

As an example, a public equity manager for TRS set a goal of engaging companies comprising at least 70% of Scope 1 and 2 financed emissions for the System’s assets and seeks to increase this target to 90% of Scope 1, 2 and 3 financed emissions by 2030. The manager will identify companies in high-emitting sectors to prioritize engagement and place emphasis on engaging companies to adopt quantified climate ambitions. The manager recognizes in its engagements that progress on adoption and implementation of increasingly mature decarbonization practices may take time to accomplish. The manager will follow up at least annually with holdings to track their progress or consider other action as appropriate.

A fixed income manager for TRS, developed a method of prioritizing companies for engagement that are among those in the portfolio with the highest emissions intensity. They will create a priority list of 20-30 companies focused on highest emitters by sector that do not have science-based targets. This list is expected to correspond to 70% of the portfolio’s total emissions intensity. The manager will annually monitor companies’ progress and assess if companies subject to engagement constitute 70% of the portfolio’s weighted average carbon intensity.

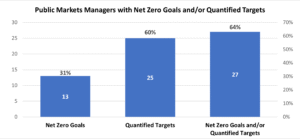

The following graph shows the numbers and percentages of managers that adopted net zero goals and/or quantified engagement or portfolio targets.

Note: Net Zero Goals include managers with science-based targets.

- A substantial majority, 64% or 27, of the System’s public markets managers adopted net zero goals and/or quantified engagement or portfolio targets that apply to the System’s assets.

- 60% or 25 of public markets managers adopted quantified engagement targets. This means the manager adopted targets identical or similar to those recommended by NZIF, i.e., engaging 70% of financed emissions (Scope 1 & 2) of investments increasing to 90% of financed emissions (Scope 1, 2 & material 3) by 2030.

- 31% or 13 of public markets managers adopted net zero goals.

- The number of managers with net zero goals and/or quantified targets is fewer than the sum of managers with net zero goals and managers with quantified targets. This is because some managers have both net zero goals and quantified targets.

- Two managers with net zero goals do not yet have quantified targets but are actively exploring the development of such targets.

- 14 managers have quantified targets but do not have net zero goals.

- The total number of managers that have quantified targets includes four funds of funds managers. BAM counts these managers as having quantified targets based on their plans to engage 100% of their submanagers on the net zero expectations.

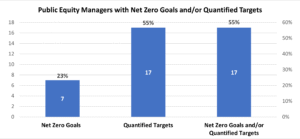

The next two graphs show the numbers and percentages of managers with net zero goals and/or quantified engagement or portfolio targets broken down by public equity and fixed income managers. Please note the sum of the managers from the two following graphs exceeds 42, the total number of TRS’ public markets managers. The reason for this is some managers have mandates with TRS to invest in both public equity and fixed income. TRS has 31 managers for public equity mandates and 16 managers for fixed income mandates. BAM assessed all managers for how they approached all applicable mandates.

The following graph shows the numbers and percentages of managers in Public Equity that adopted net zero goals and/or quantified engagement or portfolio targets. TRS has 31 total managers that manage public equity mandates for the System.

- A majority, 55% of or 17 of the System’s public equity managers adopted net zero goals and/or quantified engagement or portfolio targets that apply to the System’s assets.

- 55% of or 17 public equity managers adopted quantified engagement targets.

- 23% or seven public equity managers adopted net zero goals.

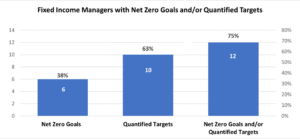

The following graph shows the numbers and percentages of managers in Fixed Income that adopted net zero goals and/or quantified engagement or portfolio targets. TRS has 16 managers that manage fixed income mandates for the System.

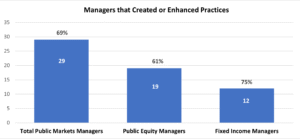

Substantial Majority of Managers Created New Practices or Enhanced Existing Practices

Most managers created new policies or practices or enhanced existing policies or practices, consistent with fiduciary standards, to meet the System’s net zero expectations. The following graph shows the numbers and percentages of managers that created or enhanced policies or practices because of BAM’s engagement on the System’s behalf.

Note: The percentages shown are only for the corresponding category of managers.

- A substantial majority – 69% or 29 – of the System’s total public markets managers created new policies or practices or enhanced existing policies or practices as a result of the System’s expectations.

- A substantial majority of public equity managers – 61% or 19 of public equity managers – created or enhanced policies or practices.

- A substantial majority of fixed income managers – 75% of 12 of fixed income managers – created or enhanced policies or practices.

- Seven of the 13 public markets managers that have net zero goals for the System’s assets adopted these goals because of the System’s net zero expectations.

For example, the quantified targets set by the public equity and fixed income manager examples described above are newly created practices established because of the System’s net zero expectations. The new or enhanced practices of other managers commonly include measuring and reporting financed emissions, conducting new or additional tracks of engagement of companies to support decarbonization, and assessing and monitoring the net zero alignment of companies. The System’s fund of funds managers in Public Equity and Fixed Income also created new practices to communicate the System’s net zero expectations to their submanagers and assess, engage and monitor submanagers on their decarbonization efforts and progress.

3.2. Monitoring and Engagement of Managers’ Assessment of Climate-Related Risks and Opportunities

BAM regularly monitors and assesses managers on environmental, social, and governance (ESG) policies and practices, including climate-related practices, with an annual ESG questionnaire. The questionnaire includes specific questions related to climate and net zero alignment on topics such as:

- Measurement and reporting of Scope 1, 2, and 3 GHG emissions

- Utilizing decarbonization as a strategy for value creation

- Assessment of the resilience of portfolio companies or assets in different warming scenarios

- Assessment of physical climate risk, transition risk, biodiversity-related impacts and dependencies, deforestation risk, water-related risk and environmental justice.

BAM received responses from 148 managers for 347 funds (including public markets and private markets funds) that represent 94% of TRS’ AUM.

For GHG emissions disclosure, about 38% of responsive managers (across public and private markets including passive and active investments) covering 29% of TRS AUM stated they measure and report Scope 1 and 2 emissions for all investments. 30% of these managers covering 23% of the AUM stated they measure and report Scope 3 emissions for all investments.

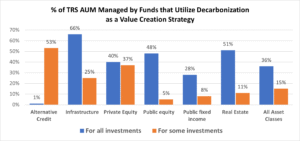

3.2.1. Decarbonization as a Strategy for Value Creation

Many of TRS’ managers use decarbonization as a strategy for value creation as shown by the following graph per the percentages of TRS’ AUM across all asset classes.

3.2.2. Assessment of Physical Climate Risk

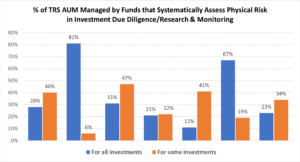

The following graph shows the percentages of TRS’ AUM that report systematic assessment of physical climate risk in investment due diligence, research and monitoring across all asset classes. Physical climate change risks include risks to property, assets, infrastructure and business operations from extreme weather events and longer-term changes and variability in weather, weather patterns and associated conditions.

A substantial majority of the AUM in real estate and infrastructure is managed in funds that systematically assess physical risk in investment due diligence, research, and monitoring. BAM addresses physical climate risk assessment when conducting due diligence, monitoring and engagement of asset managers, particularly in the real estate and infrastructure asset classes.

3.2.3. Assessment of Climate Transition Risk

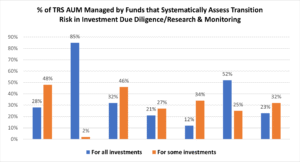

The following graph shows the percentages of TRS’ AUM that report systematic assessment of climate transition risk in investment due diligence, research, and monitoring in all asset classes. Transition risks are those associated with the transition to a lower-carbon economy such as changes in technology, policy, market conditions and consumer preferences. This includes the risks of higher emissions in a company’s or asset’s business activities and value chain.

Real estate and infrastructure funds also lead the asset classes in terms of systematically assessing transition risks with 85% of infrastructure funds and 52% of real estate funds conducting this assessment for all investments. Mitigating and managing transition risk is central to the System’s net zero goals to encourage decarbonization across its portfolio. BAM will continue to engage managers and funds to encourage appropriate assessment of transition risk.

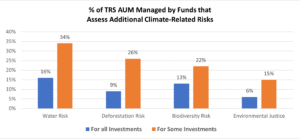

3.2.4. Assessment of Additional Climate-Related Risks: Water, Biodiversity, Deforestation & Environmental Justice

The following graph shows the percentages of TRS’ AUM that report assessment of water-related risk, biodiversity-related impacts and dependencies, deforestation risk, and environmental justice.

Among these risks, the most systematic assessment is conducted for water risk followed by biodiversity and deforestation risks.

3.2.5. Additional Manager Engagement Activities

BAM continues to engage managers to encourage and support further adoption of net zero goals, science-based targets or other appropriate decarbonization goals. In addition, BAM will seek to further understand managers’ integration and pricing of physical, transition, nature, and water risks.

BAM has increased its participation and collaborative work, on behalf of the System, in industry initiatives to support net zero alignment with asset managers across asset classes. For example:

- BAM co-hosted a half-day workshop for middle market private equity managers (general partners (GPs)) during New York Climate Week 2025 to provide guidance on portfolio decarbonization and value creation. BAM co-hosted the event with three other limited partners (LPs) (APG, PGGM and AlpInvest). Approximately 50 GPs participated and provided positive feedback on the workshop citing helpful features such as GP decarbonization examples, networking opportunities and LP perspectives. BAM plans to co-host the event again in 2026.

- In 2024-2025, BAM participated in a working group of LPs to develop a set of climate-related due diligence questions to support LPs in assessing how private equity managers govern and manage climate-related risks and opportunities. This initiative was led by the Principles for Responsible Investment (PRI) in collaboration with the Institutional Limited Partners Association (ILPA) and Initiative Climate International. The due diligence questions are titled “PRI Supplementary Climate Module” and were released in November 2025. As of January 2026, BAM incorporated the questions of the Module in its supplemental due diligence questionnaire while adapting them to be more in-depth in certain areas as well as applicable more broadly for private markets.

- In 2025, BAM joined the ESG Data Convergence Initiative (EDCI), a global consortium of LPs and GPs formed to promote industry-wide convergence towards a standardized, foundational set of ESG metrics, including key climate metrics, in private markets. EDCI provides GPs with a process to report a core set of ESG data from their portfolio companies and make this data available to LPs. EDCI also creates a benchmark for this data enabling LPs and GPs to compare the ESG performance of their investments and identify correlations between ESG performance and value creation. EDCI enables reporting for each portfolio company on: (1) Scope 1, 2 and 3 GHG emissions (2) whether it has a decarbonization strategy/plan, (3) whether it has a short-term GHG emissions reduction target (Paris-aligned or non-Paris-aligned), (4) whether it has a long term net zero goal, (5) total energy consumption and (6) total renewable energy consumption.

3.3. Due Diligence of Asset Managers

BAM conducts due diligence of material ESG factors, including climate change-related risks and opportunities, for all asset managers across all asset classes as part of the overall diligence process conducted prior to recommendations and approvals of investments to the Board. Climate change poses both systemic and idiosyncratic risks for the investment portfolio and is, therefore, actively assessed in the diligence for all managers and strategies and explored in more depth where it may be more financially material.

As a starting point for diligence, BAM utilizes the Due Diligence Questionnaire template of the ILPA for private markets managers and a similar template for public markets managers. BAM supplements the ILPA-based template with a BAM-specific due diligence questionnaire (BAM DDQ) that includes additional questions on ESG and climate. Using both questionnaires, BAM assesses how managers consider climate change-related risks and opportunities, including physical risk and transition risk, in diligence and portfolio management. BAM also asks whether and how managers measure the GHG emissions (including Scopes 1, 2 and 3) of their investments and whether managers have specifically adopted net zero goals, science-based targets or other emissions reduction targets for their investments. During diligence, the BAM team meets with the managers to gain additional insights and explores managers’ climate-related approaches in greater depth, particularly for higher-emitting investments.

As mentioned above, as of January 2026, BAM updated its BAM DDQ with an adaptation of the PRI Supplementary Climate Module to ask more specific questions on how GPs approach climate-related issues in due diligence, post-investment and reporting/disclosure. For example, the BAM DDQ now delves further into how the GP approaches climate-related value creation, assessment of physical risks, resilience and adaptation for physical risks, climate-related KPIs and portfolio level climate risk analysis, including climate scenario analysis. BAM further updated the questionnaire to ask about managers’ approaches to assessing nature/biodiversity impacts and dependencies. BAM summarizes and reports findings related to climate-related ESG diligence in investment memoranda to the Board.

Section 4: Invest in Climate Change Solutions

4.1. Progress on Climate Solution Investments

TRS’ investment in climate solutions has been an integral part of our net zero ambitions. TRS has a goal of investing a total of $19 billion in climate change solutions by 2035, and had an interim goal of $4.2 billion by 2025, consistent with our fiduciary duties and our investment objectives. TRS surpassed the goal set for 2025, earlier, in June 2024. As of June 30, 2025, TRS has a total of $7.34 billion in invested and unfunded commitments in climate change solutions across all asset classes, an increase of 24.4% over FY2024. Table 4 shares the climate solutions exposure by each asset class for Jun 30, 2025, as well as changes from FY2024.[15]

Details of TRS’ climate solutions investments’ definitions by asset class are in Appendix D.

Table 4: TRS Climate Solutions Investments – Jun 2025

| TRS – Climate Solutions Investments ($million) – Jun 30, 2025 | ||||||||

| Total Portfolio | Public Equity Active | Public Equity Passive | Public Fixed Income | Alternative Credit | Private Equity | Real Estate | Infrastructure | |

| 2Q 2025 (Including unfunded commitments) | ||||||||

| 06/30/25 total NAV | 113,894 | 18,168 | 34,680 | 37,472 | 4,803 | 8,862 | 6,307 | 3,603 |

| 06/30/25 climate exposure | 7,342 | 706 | 3,639 | 792 | 229 | 324 | 707 | 945 |

| 06/30/25 climate % | 6.45% | 3.88% | 10.49% | 2.11% | 4.77% | 3.66% | 11.21% | 26.23% |

| TRS – Climate Solutions Investments ($million) – Jun 30, 2024 | ||||||||

| Total Portfolio | Public Equity Active | Public Equity Passive | Public Fixed Income | Alternative Credit | Private Equity | Real Estate | Infrastructure | |

| 2Q 2024 (1Q24 data for infrastructure; 4Q23 data for real estate) – Including unfunded commitments | ||||||||

| 06/30/24 total NAV | 105,104 | 17,607 | 29,307 | 36,514 | 4,197 | 8,979 | 5,663 | 2,837 |

| 06/30/24 climate exposure | 5,904 | 626 | 2,722 | 816 | 152 | 276 | 655 | 657 |

| 06/30/24 climate % | 5.62% | 3.56% | 9.29% | 2.23% | 3.62% | 3.07% | 11.56% | 23.16% |

| Analysis of Changes from Jun 2024 to Jun 2025 | ||||||||

| Total Portfolio | Public Equity Active | Public Equity Passive | Public Fixed Income | Alternative Credit | Private Equity | Real Estate | Infrastructure | |

| Total NAV % Change | 8.4% | 3.2% | 18.3% | 2.6% | 14.4% | -1.3% | 11.4% | 27.0% |

| Climate exposure % Change | 24.4% | 12.7% | 33.7% | -2.9% | 50.8% | 17.6% | 8.0% | 43.8% |

While this demonstrates strong progress towards TRS’s established goals, TRS is reflecting on how we can be more intentional in its climate solution investments. The climate solutions definitions for public companies have evolved since TRS set its climate solutions investments target four years ago. In 2023, the methodology changed from only companies with more than 50% revenue from green categories to including the proportion of investments based on the companies’ green revenue percentage based on MSCI’s Environmental Impact Metrics. Two years on, the increasing urgency of climate change requires us to be more intentional in our climate solution investments and seeking high performing assets. The market has also evolved. Given these drivers, we provide more granular reporting on the make-up of our climate solution investments in this report, starting with the private real estate and public markets. We are also reviewing peer asset owners’ practices on climate solutions investments to make sure we adhere to the best practice. Going forward, we aim to focus our effort on investments that have the highest effect on emission reduction while also providing superior risk adjusted returns.

4.2. Review of Inclusion of Products and Services Associated with Data Centers as Climate Solutions

TRS has been monitoring the increasing emissions of artificial intelligence (AI)-driven data center growth, which are projected to increase significantly in coming years. Accenture research, for example, found that carbon emissions from AI data centers could increase 11-fold in this decade, accounting for a 3.4% share of total global CO2 emissions by 2030 and more than the aviation industry’s current share of emissions[16].

Because cloud computing is more energy efficient than local servers which was prevalent a decade ago when MSCI designed its methodology, to date, MSCI has categorized revenues from products and services associated with cloud computing which AI relies on as contributing to energy efficiency, hence part of the environmental impact metrics,[17] We currently define climate solution investments using MSCI’s environmental impact metrics. This means that a significant portion of the investments associated with AI are designated as climate solutions. For example, MSCI classifies 88% of Nvidia’s revenue as contributing to energy efficiency, hence 88% of TRS’s investment in Nvidia is classified as a climate solution investment. Nvidia is currently the largest single contributor to TRS’s climate solutions. Nvidia, Microsoft, and Amazon combined comprise almost 30% of TRS total climate solutions (both public and private combined) in FY 2025.

Given the significant climate impact of AI, TRS began reviewing the inclusion of related forms of revenue in its climate solutions portfolio and engaging with both hyperscalers and other portfolio companies on this issue (see additional detail in the corporate engagement section). Additionally, TRS has requested that MSCI review its environmental impact metrics definitions as well and has committed to participate with other investors in such a review. The results of these reviews and engagements will inform potential changes to TRS’s definitions (and reporting) of climate solutions.

4.3. Review of Private Real Estate Climate Solution Investments

Up until FY 2024, we defined real estate climate solutions as buildings that achieve Energy Star certification. Energy Star certification is based on a building’s energy efficiency and requires a score of 75 or higher, regardless of whether they are existing buildings, new builds, or major renovations, placing it in the top 25% of all Energy Star-rated buildings. However, Energy Star certification is generally limited to buildings in the U.S. and Canada and does not capture high-performing buildings in Europe in the System’s portfolio. What’s more, because of the higher building standards for new buildings, most new buildings have an Energy Star rating of 75 or above.

For FY 2025, we collected additional indicators for building energy performance to expand our understanding of high-performing assets in our real estate portfolio. Specifically, in late 2025, we expanded the climate-related data collection from our real estate managers to include the Energy Performance Certificate (EPC) levels for European properties.

Furthermore, we have begun to examine standards for higher levels of building energy efficiency performance to assess and differentiate how the System’s real estate investments are with this performance. One established standard is the Climate Bonds Initiative’s green bond eligibility criterion for residential buildings. This criterion requires performance in the top 15% of similarly located buildings.[18] BAM applied this concept of the top 15% to analyze the EPC levels of buildings in the System’s portfolio and found that, for the countries in which the System has real estate investments, existing buildings, as opposed to newly developed buildings, with the top two EPC ratings (e.g., A or B for the UK, A+ or A for Germany), outperform around 85% of similar buildings. Because of the high energy efficiency requirements for new buildings in Europe, most new buildings have the top two ratings. To be consistent with the U.S. real estate climate solution definition, we counted both new buildings and existing buildings in Europe with the two top ratings as climate solutions in the headline numbers in Table 4.

While we currently retain the definition of real estate climate solutions as the top 25% in Energy Star ratings for U.S. properties, in this report, we begin to report additional data on higher performing real estate investments to provide more helpful insights into the System’s real estate investments that contribute to the transition to a net zero economy. Specifically, we report (1) real estate investments in European existing buildings achieving the top two EPC ratings and (2) U.S. real estate investments with Energy Star ratings of 85 or higher indicating they perform in the top 15%. Combined, these two categories of investments total $356 million which is 6% of the real estate portfolio NAV as of June 30, 2025. This is about half of the total NAV of the headline real estate climate solutions total investments.

| US Existing Buildings with 85+ Energy Star Ratings | European Existing Buildings with Top Two EPC Levels | |

| Higher Performing Real Estate Climate Solution Investments | $245mm | $115mm |

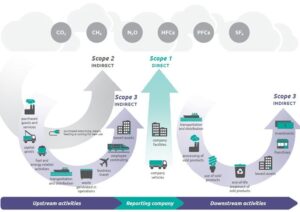

Appendix A – Definitions of GHG Emissions and their Categories (Scopes 1, 2 and 3)

Scopes 1, 2 and 3 are ways of categorizing the different sources of GHG emissions from a company’s direct operations and its wider value chain.

| Scope 1 | Scope 2 | Scope 3 |

| Covers the direct emissions from sources owned or controlled by a company – for example, by running its boilers and vehicles | Covers indirect emissions from the generation of energy a company purchases | Covers all other indirect emissions up and down a company’s supply and value chain. For example, a petroleum company’s Scope 3 emissions include the emissions from the gasoline they produce when it is burned by a customer’s car. A bank’s Scope 3 emissions include those from extracting fossil fuels from projects they finance. It is estimated that Scope 3 emissions constitute 75% of firms’ emissions on

average10. |

Illustration of Scopes 1, 2 and 3 emissions

Source: Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)

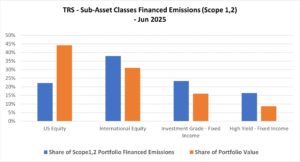

Appendix B – Scope 1,2 Absolute Financed Emissions Breakdown

As of June 30, 2025, total public equity and corporate bonds represent about 75% and 25% of the measured public security portfolio’s market value, but their contributions to Scope 1 and 2 financed emissions are 60% and 40%, respectively. U.S. equity has higher total financed emissions but lower financed emissions intensity than international equity. Within fixed income, high yield has lower total financed emissions but higher emissions intensity than investment grade corporate bonds.

Fig 1: Sub-Asset Classes Absolute Financed Emissions (Scope 1 and 2)

Jun 30, 2025

Between June 2024 and June 2025, the Scope 1 and 2 financed emissions from public equity decreased for the TRS portfolio, while those of fixed income increased.

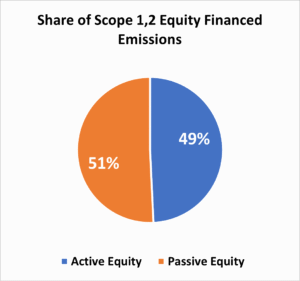

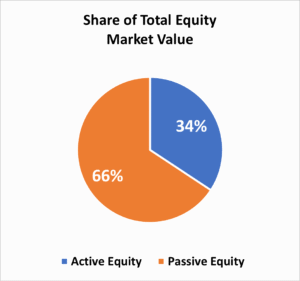

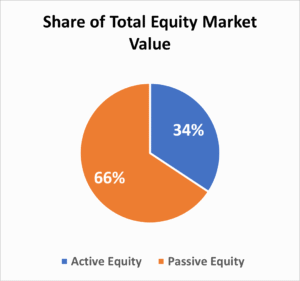

While the portfolio’s total passive equity market value is much greater than the active equity market value, the contribution of actively managed equity to Scope 1 and 2 financed emissions is not far off that of the passive equity.

Fig 2: Active vs Passive Equity Absolute Financed Emissions (Scope 1 and 2)

Jun 30, 2025

Between June 2024 and June 2025, the decrease in active public equity financed emissions was the primary driver of the overall portfolio’s financed emissions reduction, though passive equity financed emissions decreased too.

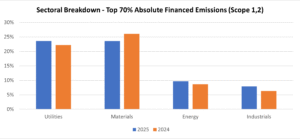

The top 70% of Scope 1 and 2 financed emissions are attributed to 200 issuers in the TRS portfolio, and the high emitting sectors in the top 70% financed emissions companies mirror the overall portfolio’s high emitting sectors.

Fig 3: Sector Contribution – Top 70% Financed Emissions (Scope 1 and 2)

Jun 2025 and Jun 2024

The Utilities and Materials sectors are the highest emitting sectors among the top 70% of Scope 1 and 2 financed emissions, representing 24% and 24% financed emissions of the group, respectively. This information continues to be critical to our engagement activities.

As shown below, the Weighted Average Carbon Intensity (WACI) (financed emissions per million dollars of sales) decreased by 5.74% for Scopes 1,2 during the year 2024-2025.

Table 1: WACI – Scope 1 and 2

| TRS – Weighted Average Carbon Intensity – Scope 1 and 2 | ||

| TRS Portfolio Tons carbon emissions/$m sales |

Blended Benchmark Tons carbon emissions/$m sales |

|

| 31-Dec-19 | 233.12 | 185.33 |

| 30-Jun-22 | 172.35 | 177.70 |

| 30-Jun-23 | 156.10 | 176.00 |

| 30-Jun-24 | 132.30 | 153.70 |

| 30-Jun-25 | 124.70 | 148.90 |

| Change % (2019-2025) | -46.51% | -19.66% |

| Change % (2024-2025) | -5.74% | -3.12% |

Appendix C – Scope 3 Absolute Financed Emissions Breakdown

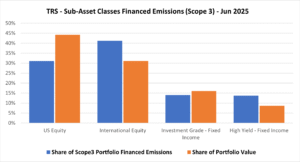

As of June 30, 2025, public equity and corporate bonds represent approximately 75% and 25% of the combined market value, with their contributions to Scope 3 financed emissions are 72% and 28%, respectively. U.S. equity has lower Scope 3 financed emissions and lower emissions intensity than international equity. Within corporate bonds, high yield has much higher total financed emissions intensity, but similar total financed emissions than investment grade corporate bonds.

Fig 1: Sub-Asset Classes Financed Emissions (Scope 3) – Jun 30, 2025

Between June 2024 and June 2025, the Scope 3 finance emission of public equity financed emissions decreased for the TRS portfolio, while overall fixed income’s financed emissions increased.

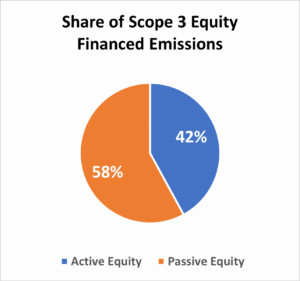

While the portfolio’s total passive equity market value is much greater than the active equity market value, the contribution of actively managed equity to Scope 3 financed emissions is not far off from that of the passive equity.

Fig 2: Active vs Passive Equity Financed Emissions (Scope 3) – Jun 30, 2024

Between June 2024 and June 2025, the decrease in active public equity financed emissions was the primary driver of the overall portfolio’s financed emissions reduction.

Table 1: WACI – Scope 3

| TRS – Weighted Average Carbon Intensity – Scope 3 | ||

| TRS Portfolio Tons carbon emissions/$m sales |

Blended Benchmark Tons carbon emissions/$m sales |

|

| 30-Jun-22 | 642.40 | 809.30 |

| 30-Jun-23 | 647.90 | 792.00 |

| 30-Jun-24 | 589.50 | 737.90 |

| 30-Jun-25 | 587.50 | 752.90 |

| Change % (2024-2025) | -0.34% | 2.03% |

WACI (financed emissions per million dollars of sales) decreased slightly by 0.34% for Scope 3 during the year 2024-2025.

Appendix D – Current Climate Solutions Investments Definitions

Public Equity: Companies that derive revenue from MSCI’s Environmental Impact categories of alternative energy, energy efficiency, green building, pollution prevention, or sustainable water. New weighted average method adopted as of 4Q 2022.

Public Fixed Income: Companies that derive revenue from MSCI’s Environmental Impact categories of alternative energy, energy efficiency, green buildings, sustainable water, pollution prevention, or sustainable agriculture, as analyzed by Risk Management. New weighted average method adopted as of 4Q 2022.

Also includes green bonds based on manager surveys conducted by Fixed Income Team. Managers were allowed discretion in defining green bonds.

Alternative Credit: OFI market values are based on manager surveys conducted by Alternative Credit Team. The definition of climate solutions used for OFI is “investments in companies that generate 50% or more revenue from clean and renewable energy technologies and assets including (1) renewable energy such as solar, wind, geothermal and hydropower; (2) energy efficiency and energy smart technologies such as power storage, fuel cells and carbon capture and storage; (3) energy efficient transport and (4) low carbon buildings.” This definition is a summary of the MSCI and Burgiss definitions as well as a reflection of a definition by Ceres. Total OFI NAV based on data from Alternative Credit Team.

Private Equity: Companies predominantly focused on a business activity classified under the Burgiss category of “Eco Friendly” activities, including renewable energy, biofuel and other clean tech or associated companies. All data is NAV. We also included companies that largely aligned with our definition of climate solutions in public markets.

Real Estate: Properties certified as Energy Star or having a score above 75 for US properties and having the top two ratings of the Energy Performance Certificate of the corresponding countries for European properties. Includes properties certified as LEED only if they are also certified as Energy Star. All data is based on manager surveys conducted by the Real Estate Team. All data is NAV.

Infrastructure: Includes categories of alternative energy, energy efficiency, green buildings, sustainable water, pollution prevention, and sustainable agriculture.

Economically Targeted Investments (ETI): ETI data is incorporated in the data for Public Fixed Income and Real Estate due to the portfolio’s investment structure.

The calculations include only assets for which BAM provides investment advice and, therefore, does not include VSFs.

Endnotes

[1] MSCI’s Total Portfolio Footprinting (TPF) methodology was used to obtain PCAF-aligned emissions metrics for Scopes 1 and 2 in 2025. However, we used MSCI’s legacy Carbon Footprint Calculations for Scope 3 this year given challenges we experienced in TPF. TPF is a relatively new tool developed by MSCI and is still a work in progress. We strive for the highest data and analytic quality and will review and update the methodologies as the carbon footprinting field evolves.

[2] https://www.iea.org/reports/global-energy-review-2025/co2-emissions

[3] Net Zero by 2050 – Analysis – IEA

[4] Applying the same methodology as MSCI’s ‘Framework for Attributing Changes in Portfolio Carbon Footprint

[5] Greenhouse Gas Protocol Scope 3 Frequently Asked Questions

[6] Material, But Missing: Gaps in Scope 3 Reporting Persist | MSCI

[7] IIGCC Investor Approaches to Scope 3

[8] The Steel Climate Standard – Global Steel Climate Council

[9] https://cdn-dynmedia-1.microsoft.com/is/content/microsoftcorp/microsoft/msc/documents/presentations/CSR/2025-Microsoft-Environmental-Sustainability-Report-PDF.pdf

[10] https://sustainability.aboutamazon.com/2024-report

[11] https://www.gstatic.com/gumdrop/sustainability/google-2025-environmental-report.pdf

[12] These expectations apply only to public markets managers that manage public equity or corporate bonds for the System including actively and passively managed public equity, investment grade credit and high yield fixed income. They do not currently apply to managers that manage Treasuries or Mortgages.

[13] Comptroller Lander Recommends Pension Boards Drop BlackRock, Fidelity, and PanAgora Due to Inadequate Decarbonization Plans – Office of the New York City Comptroller Mark Levine

[14] While PMDR specifically addresses private markets, it provides a reporting protocol and decarbonization maturity scale that can also information public markets decarbonization approaches.

[15] For real estate climate solutions, we expanded our coverage of managers that were reporting since last year, by including European assets.

[16] Unlocking Alpha in Transactions Report | Accenture

[17] MSCI Sustainable Impact Metrics

[18] World Green Building Council Sustainable Finance factsheet series – Energy Performance Certificates